Payday loans are a type of short-term loan that can be used to cover unexpected expenses or bridge the gap between paychecks. While they may seem like an attractive option for those in need, payday loans come with high interest rates and fees that can quickly add up. This blog post will explore some key statistics about the payday loan industry in the United States, including revenue figures, borrower demographics, and default rates.

We’ll also look at how states have responded to this growing problem by outlawing certain types of payday lending practices. By understanding these facts and figures related to payday loans, we can gain insight into why so many Americans turn to them as a source of quick cash – but also why it’s important for borrowers to understand their rights when taking out such a risky form of credit.

This statistic is a testament to the immense size and scope of the payday loan industry in the US. It serves as a reminder of the sheer magnitude of the industry and its impact on the US economy. It also highlights the need for greater regulation and oversight of the industry to ensure that consumers are protected from predatory practices.

There are around 18,000 payday loan stores in the United States.

This statistic is a stark reminder of the prevalence of payday loan stores in the United States. It speaks to the sheer number of establishments that are dedicated to providing short-term, high-interest loans to those in need of quick cash. It is a testament to the size and scope of the payday loan industry, and the impact it has on the lives of many Americans.

Payday Loan Industry Statistics Overview

Payday loan borrowers pay an average of $458 in fees for a $350 loan annually.

This statistic serves as a stark reminder of the exorbitant costs associated with payday loans. It highlights the fact that borrowers are paying more than 130% of the loan amount in fees each year, making it difficult for them to pay off the loan and get out of debt. This statistic is a powerful illustration of the predatory nature of the payday loan industry and the need for more consumer protections.

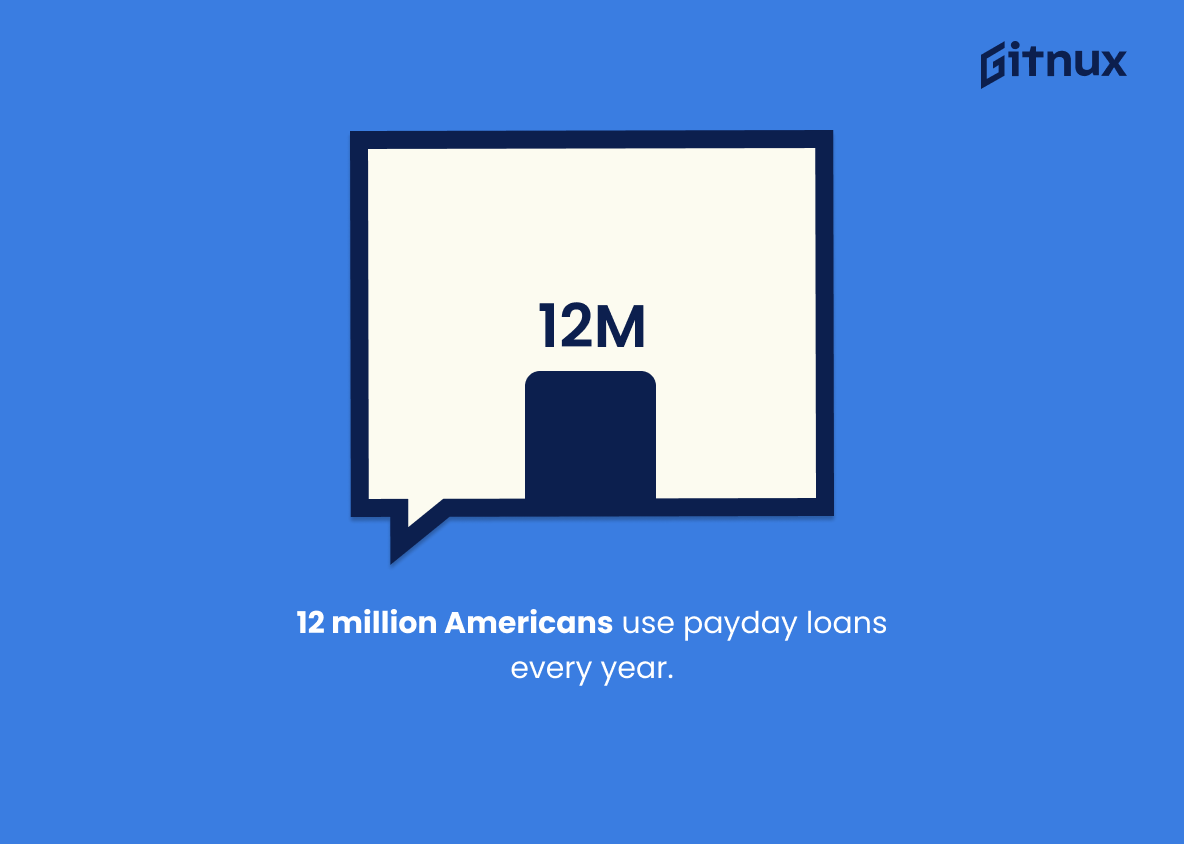

12 million Americans use payday loans every year.

This statistic is a powerful indicator of the prevalence of payday loans in the United States. It demonstrates that millions of Americans are relying on these short-term loans to make ends meet, highlighting the need for greater regulation and oversight of the payday loan industry.

80% of payday loans are rolled over or followed by another loan within 14 days.

This statistic is a telling indication of the payday loan industry’s reliance on repeat customers. It suggests that the majority of borrowers are unable to pay off their loans within the two-week period, and are instead forced to take out additional loans to cover the cost of the original loan. This statistic is a stark reminder of the potential pitfalls of payday loans, and serves as a warning to potential borrowers of the dangers of taking out such loans.

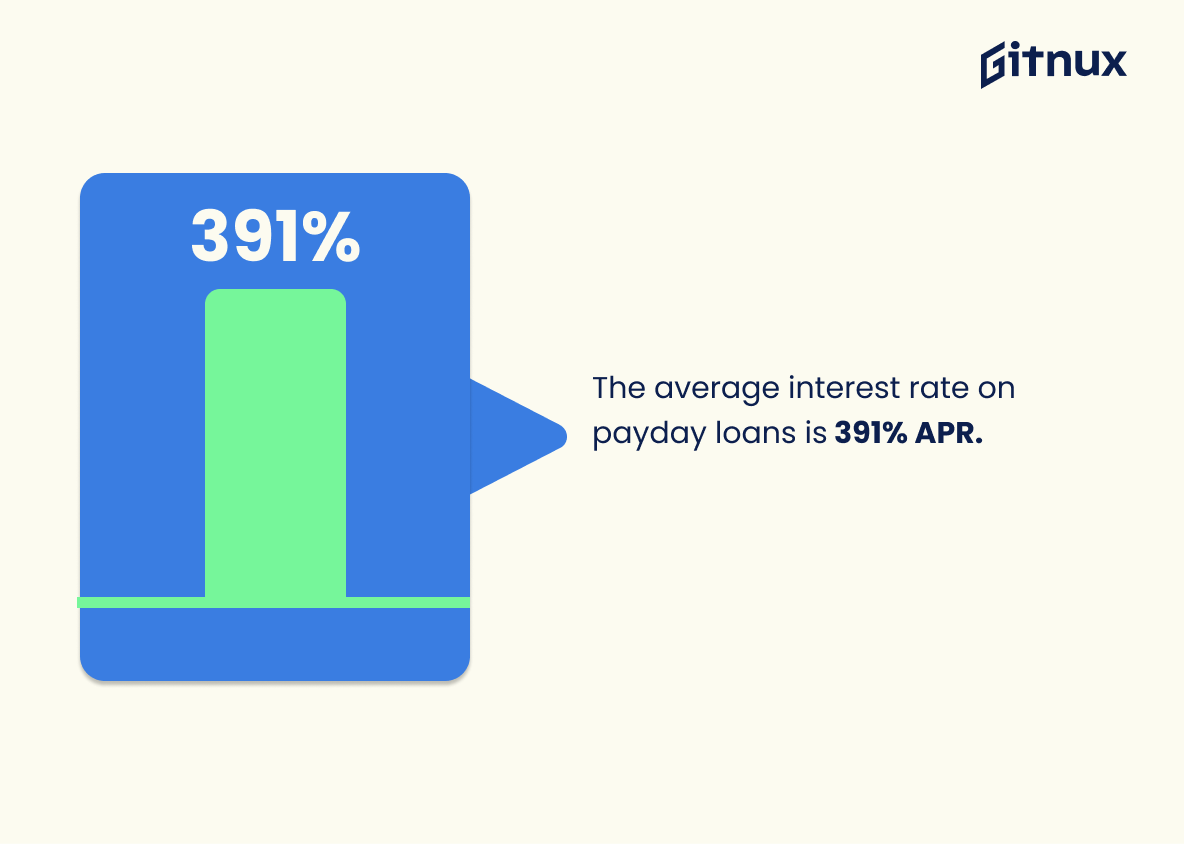

The average interest rate on payday loans is 391% APR.

This statistic is a stark reminder of the exorbitant costs associated with payday loans. It serves as a warning to potential borrowers that they should be aware of the high interest rates that come with these loans and to consider other options before taking out a payday loan. It also highlights the need for more regulation of the payday loan industry to protect consumers from predatory lenders.

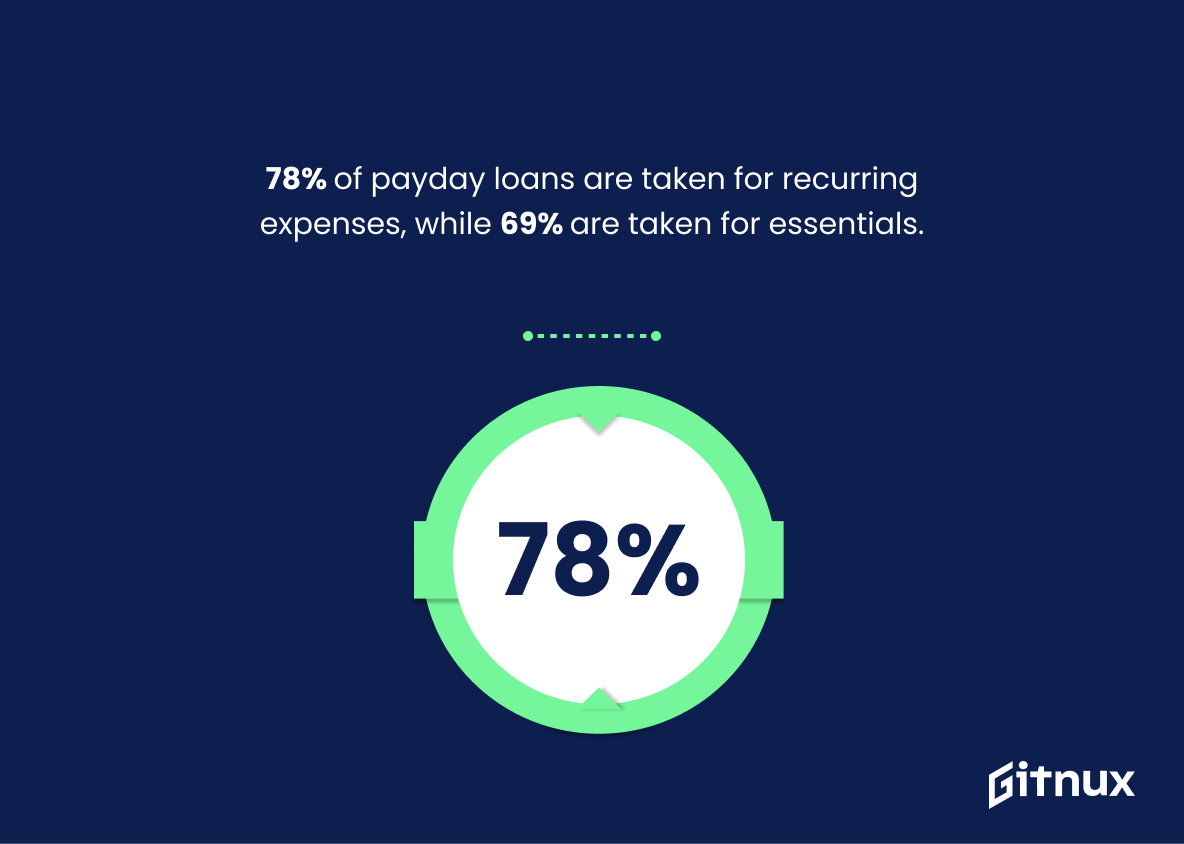

78% of payday loans are taken for recurring expenses, while 69% are taken for essentials.

This statistic is a telling indication of the role payday loans play in the lives of many people. It reveals that a large majority of payday loans are taken out to cover expenses that are necessary for day-to-day living, such as rent, utilities, and food. This statistic is a stark reminder of the financial struggles that many people face and the need for short-term loans to help them make ends meet. It is an important statistic to consider when discussing the payday loan industry and its impact on individuals and families.

Only 49% of payday loan borrowers believe it was a good decision to use payday loans.

This statistic serves as a stark reminder of the potential pitfalls of payday loans. It suggests that a significant portion of borrowers may have experienced negative consequences from taking out a payday loan, such as high interest rates, fees, and other unfavorable terms. This statistic is a powerful reminder of the importance of researching and understanding the terms of a payday loan before taking one out.

53% of payday loan borrowers end up with more than 4 loans within a year.

This statistic is a telling indication of the payday loan industry’s tendency to trap borrowers in a cycle of debt. It shows that the majority of borrowers are unable to pay off their loans within a year, and instead are forced to take out additional loans to cover the costs of the first. This is a concerning trend that highlights the need for more regulation and oversight of the payday loan industry.

Online payday loan borrowers incur an average annual percentage rate (APR) of 650%.

This statistic is a stark reminder of the exorbitant costs associated with payday loans. It highlights the fact that payday loan borrowers are paying an average of 650% APR, which is an incredibly high rate of interest. This statistic serves as a warning to potential borrowers to be aware of the high costs associated with payday loans and to consider other options before taking out a loan.

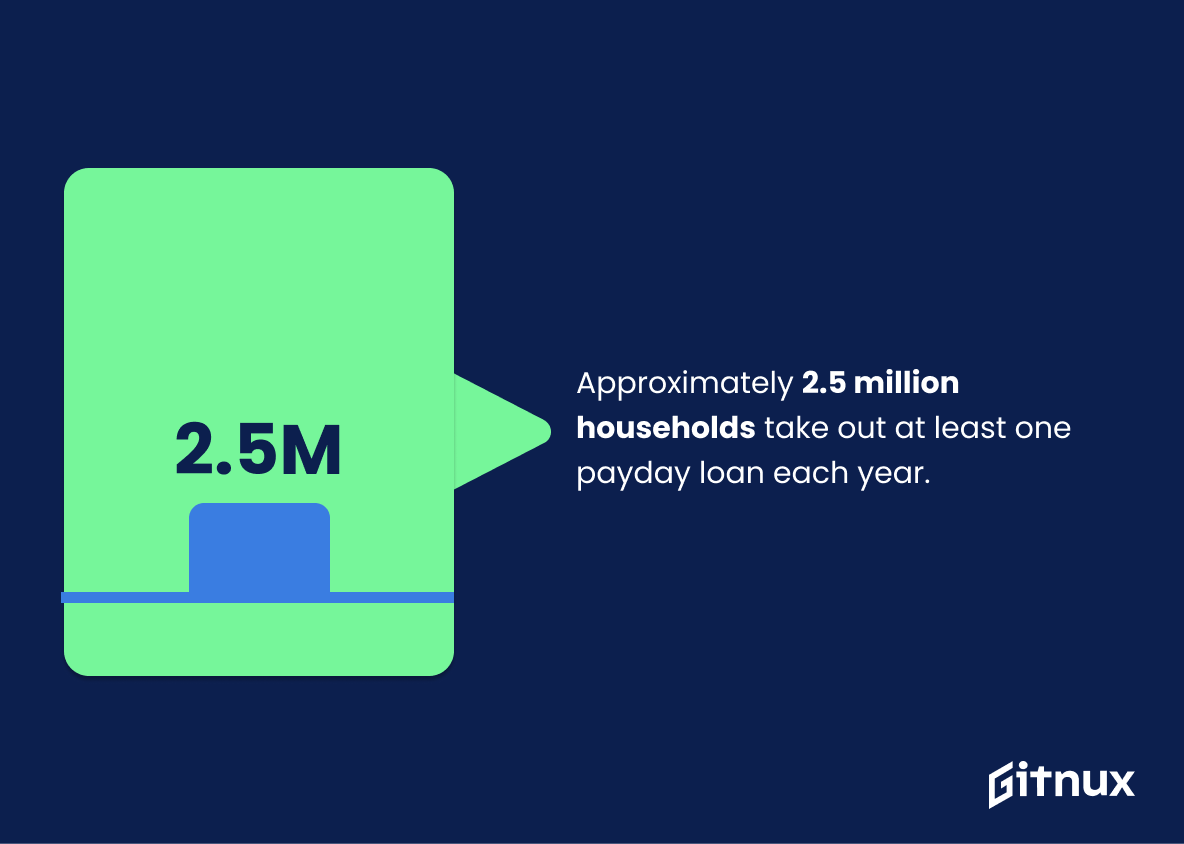

Approximately 2.5 million households take out at least one payday loan each year.

This statistic is a stark reminder of the prevalence of payday loans in our society. It shows that millions of households are relying on these short-term loans to make ends meet, highlighting the need for more accessible and affordable financial services. It also serves as a warning that the payday loan industry is growing, and that more needs to be done to protect consumers from predatory lenders.

Payday loans disproportionately impact African American and Hispanic communities.

This statistic is a stark reminder of the inequity that exists in the payday loan industry. It highlights the fact that African American and Hispanic communities are disproportionately affected by the predatory practices of payday lenders, and that these communities are more likely to be taken advantage of by lenders who are looking to make a quick buck. This statistic is a call to action to ensure that these communities are protected from the harmful effects of payday loans.

Borrowers between the ages of 25 and 49 are most likely to use payday loans.

This statistic is significant in the context of the payday loan industry because it reveals the demographic of people who are most likely to take out these short-term loans. Knowing this information can help lenders better understand the needs of their target market and tailor their services accordingly. Additionally, it can help inform policy makers and other stakeholders in the industry about the potential risks associated with payday loans and how to best protect consumers.

Approximately 27% of payday loan borrowers default on their loans.

This statistic is a stark reminder of the risks associated with payday loans. It highlights the fact that a significant portion of borrowers are unable to pay back their loans, which can lead to serious financial hardship. It is a warning sign that payday loans should be used with caution and only as a last resort.

Conclusion

The statistics presented in this blog post demonstrate the prevalence of payday loan usage and its impact on individuals, families, and communities. Payday loans are used by 12 million Americans annually, with an average interest rate of 391% APR. The majority of borrowers have lower incomes and use these loans to cover recurring expenses or essential items such as food or rent.

Unfortunately, many end up taking out multiple loans within a year due to high fees associated with rolling over existing debt. This can lead to defaulting on payments which further exacerbates financial hardship for those already struggling financially. It is clear that more needs to be done in order to protect consumers from predatory lending practices so they can access safe credit options without falling into a cycle of debt trap caused by payday lenders.

References

0. – https://www.www.nclc.org

1. – https://www.www.pewtrusts.org

2. – https://www.www.americanprogress.org

3. – https://www.www.investopedia.com

4. – https://www.www.ftc.gov

5. – https://www.www.consumerreports.org

6. – https://www.www.responsiblelending.org

7. – https://www.www.norc.org

8. – https://www.www.consumerfinance.gov

9. – https://www.www.ibisworld.com

10. – https://www.www.federalreserve.gov